An asset bubble occurs when excessive demand has buyers driving prices higher in the face of rising supply. Those rising prices become unsustainable as supply increases. Then prices drop dramatically as there are no buyers left to handle the continued supply of the asset. Remember, it is supply that bursts bubbles, not demand. So, taking a close look at these factors in our current environment, the question remains, “Are we in a new Housing Bubble Now?”

Recent headlines have bombarded us with news of the pending housing market collapse. The continued surge in home prices through the pandemic has many “experts” portraying the current environment as a housing bubble similar to the lead up to the 2008 Financial Crisis, with this news shaking real estate investments.

“Without a doubt, we are in the early stages of a housing market crash.”

“US Housing Enters 2021 In A Massive Bubble.”

“Warning: The Housing Bubble Could Get Worse.”

A review of supply and demand factors of housing will show a different situation than the doomsday headlines in the media.

The basis of modern economics is that the price of goods or labor are determined by supply and demand: the greater the demand, the higher the price; the greater the supply, the lower the price.

This is also true in housing. An accurate way to look at these economic forces is to gauge the availability (supply) of housing against its affordability (demand). The major data points of the availability are:

The relevant components of affordability are:

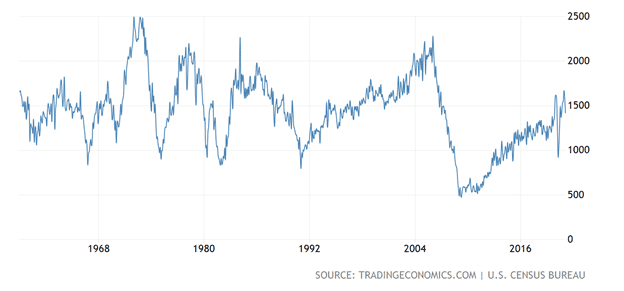

Housing Starts are the number of new residential construction projects that have started within that month. This provides a good measure of the supply of new homes that will be on the market in the coming months. They are an indicator of the health of the overall economy, with rising housing starts a sign of a growing economy.

As shown, they can be volatile on a monthly basis, primarily due to weather, but overall trends are apparent. Historically, only when starts are over two million per month do they approach an over-supply condition. While they have risen dramatically from the 2008 Financial Crisis lows, and have rebounded sharply from the pandemic lows, housing starts are not near saturation levels.

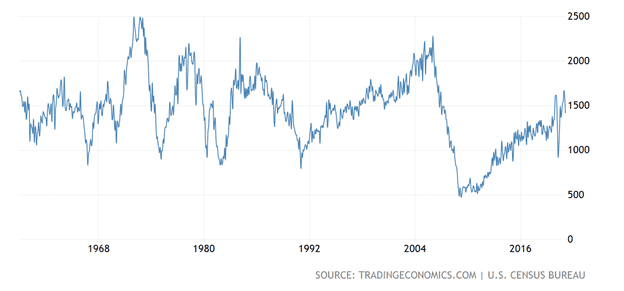

Building Permits provides the number of municipal approvals for new home construction in a single month. This is a leading indicator as permits must be approved before construction begins. This shows a similar picture to the housing starts data: that while in an upward bias, they are approaching but not at historical levels of over-construction.

The current inventory of available homes for sale is another measure of supply. This past February, that number hit a record low – just above one million homes in the entire country – that goes back to 1982.

The pandemic certainly has kept many houses from hitting the market. Contagion fears have kept some from coming to the market, while others were improved during social distancing restrictions that kept owners from searching for better homes.

Thus, we can see that while the existing inventory of available homes for sale has dramatically decreased, the number of future homes – represented by permits and starts – also has not yet hit levels of oversupply or saturation. This indicates that supply is not yet increasing enough to bubble conditions.

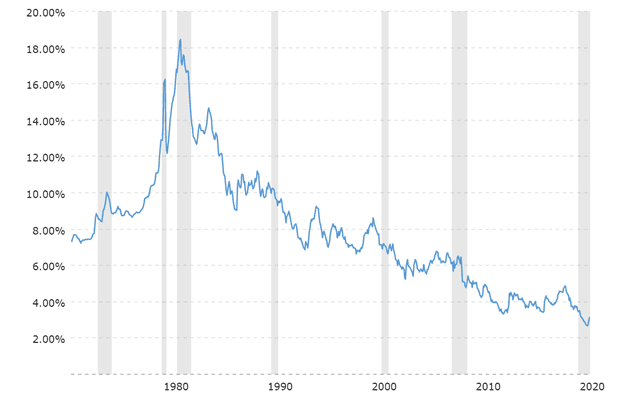

The primary driver of home purchase affordability is the level of mortgage rates. When mortgage rates are low, buyers can borrow greater amounts and thereby afford to pay higher prices. Since the early 1980s mortgage rates have steadily declined.

Despite prices steadily rising, the affordability factor has also been increasing, thus maintaining the demand.

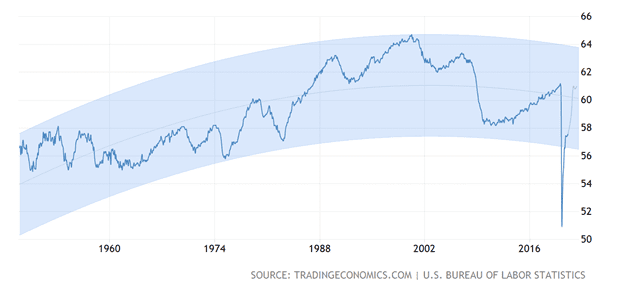

Other affordability components are wages and employment. When people have jobs with rising wages, they tend to upgrade their living standard: from rent to buy, from starter home to larger home.

While wage growth and employment have recently struggled during the pandemic to regain their pre-COVID levels, the US Bureau of Labor Statistics forecast both climbing back to or near pre-pandemic levels by 2022. Unless we hit another wave of lockdowns or enter a recession, the outlook for wages and employment are for steady growth.

While not a true factor of affordability, the population of home buyers is also an important factor of housing demand. The oft-maligned Millennials are the largest generation alive and these 25 to 40-year-olds are cresting into adulthood, families and first- or second-time home purchases.

The Financial Crisis of 2008 delayed the front end of the Millennials from purchasing, and their current demand is fueling a seller’s market, with multiple escalating and/or over-list price bids being the norm.

The last component of affordability is often overlooked, and currently may be the most significant factor guarding against a bubble. In the aftermath of the 2008 Financial Crisis, regulation of the home buying process has become more detailed and demanding, as anybody who has recently applied for a mortgage knows.

While onerous, the income verifying requirements are in stark contrast to the loose and irresponsible loan qualification processes prior to 2008. Then, the demand generated by allowing unqualified individuals to purchase houses they could not afford was obviously unsustainable. Especially in the face of the supply at that time.

The current process has placed a much greater emphasis on the borrower’s ability to repay the mortgage and not reach for a house they can not afford. This has all but eliminated “unsustainable” demand.

Housing prices have rallied significantly, especially in recent years. The larger population of potential purchaser have experienced an increase in affordability (primarily due to historically low mortgage rates) during a decrease in availability (a lack of inventory).

However, due to a lack of housing oversupply and the improved income verification of borrowers, the housing market is not in a bubble and will not be until supply exceeds excessive demand.

There are many ways to play the housing market. Homebuilder stocks may be the most direct play. Real Estate Investment Trusts (REITs) invest in a portfolio of various real estate sectors, such as Multi-family, Apartment Buildings or even Mortgages, providing diversification and high dividend payouts. Online brokers like Zillow or Redfin are gaining market share. There are also Finance companies like Rocket, IMPAC Mortgage, Fannie Mae or even the big banks like BankAmerica or Wells Fargo.

However, with the market at all-time highs, and mortgage rates increasing on growing inflation concerns, a better way to play the continued demand for housing is with lumber companies.

Almost every type of construction requires lumber. The demand has steadily increased from the lows of the 2008 Financial Crisis, with prices rising dramatically under the Trump administrations increased tariffs and soaring during the pandemic.

From the pandemic low, lumber has rocketed over 300%. Yet, most lumber company stocks have appreciated much less. There is also a lag effect before new prices are reflected in orders. This bodes well for revenue growth in the foreseeable future. A company with potential upside is Weyerhaeuser (WY).

WY is a Timber REIT, which must distribute to shareholders a minimum of 90% of taxable income in lieu of paying corporate taxes. Owning over 11 million acres of geographically diversified timberland provides risk mitigation against local forest damage.

WY’s size also enables economies of scale, keeping harvest and processing costs down and margins strong. Solid management oversees a strong balance sheet and cash flow. While up 130% from the pandemic lows, after the last lumber and market shock in 2008 the stock rallied 600% when lumber only rallied 100%. Much like the housing market, the stock is not over-extended.

Despite a seeming home buying frenzy driving prices to remarkable levels, it is the lack of supply and the quality of mortgage borrowers that prevent the current up cycle from being a housing bubble. And with expectations of continued low rates, Millennial demand and steady wage growth, a company that provides the essential construction material of lumber such as Weyerhaeuser should continue to experience revenue growth.

Wealthplicity Recent Posts