Often investors will hear about the power of compound interest or the power of compounding dividends and be confused. What does this compounding investment jargon mean and why is it one of the most important phrases you should know when you start learning how to invest.

As it relates to compound interest investments, the idea is to add any interest you earn to your investment (rather then receive it in cash), such that you receive interest not just on your original investment amount, but also any earned interest.

As a result of adding your interest earned to the original investment, the amount you earn for the next month/year will be higher. The “compounding” effects of adding earned interest to your original investment balance is to steady increase the amount of interest you earn each period.

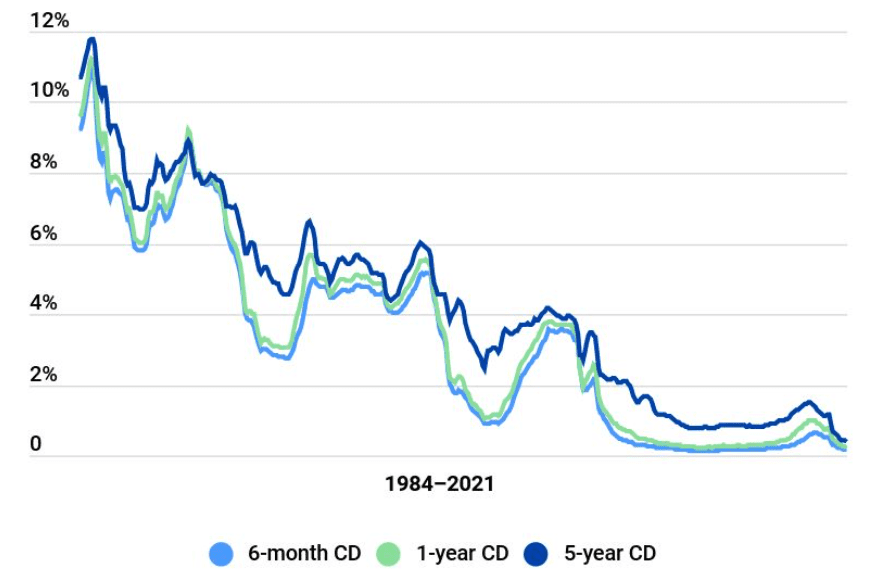

For many years, people have been sold on the benefits of opening a savings account or a Certificate of Deposit. This dates back to the 1980’s when CD’s were all the rage. But along with feathered hair and neon, they quickly went out of style.

The reason CD’s were so popular in the 1980’s was because the yield on a CD exceeded a 10% APY. If a 10% APY sounds crazy, that’s because it was. The reason interest rates were so high in the 1980’s was due to high inflation. So, even though people could enjoy double digit yields on their savings accounts, their spending power was greatly deflated.

However, fast forward to today, and the APY on a CD or a savings account is abysmal.

With rates being as low as they are today, the average APY on a CD or a savings account is below 1%. On a CD, the national average is .24% and, on a savings account, it’s even worse at .04%.

With the FED keeping rates at bay in order to reflate the economy, a savings account is one of the worst places for someone to create wealth.

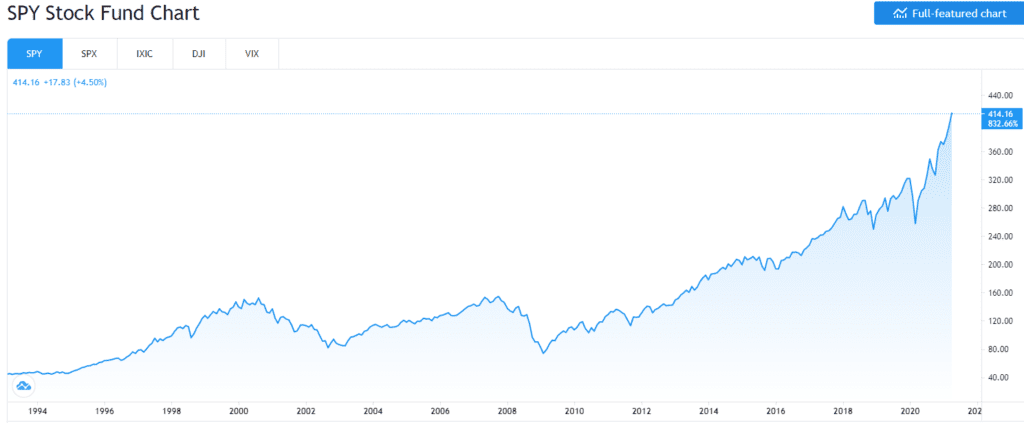

A great view is comparing the S&P 500 from the early 90’against a CD rate. While a CD APY decreased from 10% to .24%, the SPY index fund of the S&P 500, grew an astonishing 833%.

Where would you rather have your money?

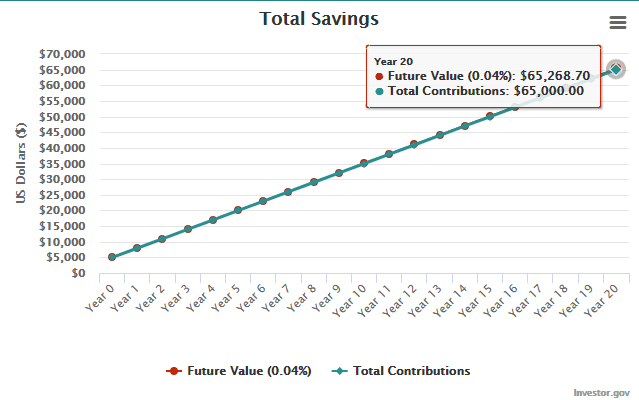

In fact, let’s take a look at scenario with some real dollars.

Let’s compare Person A who deposited $5,000 in a savings account and contributes $250 per month vs. Person B who invested $5,000 in an investment portfolio and also contributes $250 per month. And then we’ll take a look at their returns over a 20-year period.

As you can see below, the person who put their $5,000 in a savings account, then contributed $60,000 over 20 years earned an amazing $268.70 on a .04% APY. Now, that APY will most likely fluctuate, but for illustrative purposes, let’s just use the current national average.

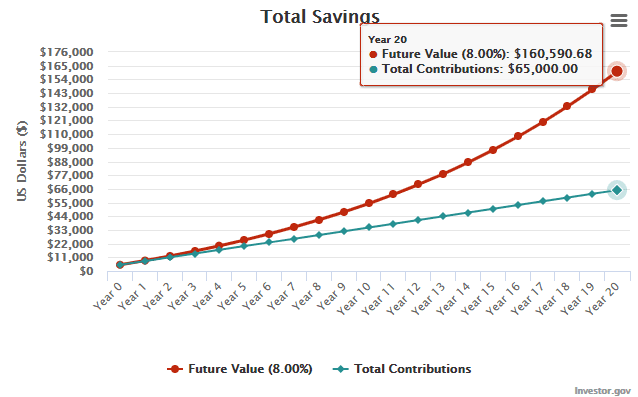

Now, let’s take a look at Person B, who invested the same amount – a $5,000 deposit and $250 monthly recurring deposit for a total of $65,000. Only, this time, instead of earning .04% APY on a savings account, they earned 8% compounding interest each year. Again, we’ll use historical averages to illustrate our point.

The difference is pretty obvious. Person B, the investor earned $160,000 more than Person A, the saver. It doesn’t even sound feasible, but that truly is the power of compounding interest.

The idea around compound interest is not new. In fact, it goes back almost 4,000 years to the Old Babylonian period (2000-1600 BC). So even then people knew of the power of “interest on interest” and some of the power it has on mathematical and investing theory.

Very much related to compounding interest rates is the idea of the “rule of 72”. This is the idea that if you are using compounding interest rates, then you can easily tell how many years it will take to double your money. This can be done by dividing your interest rate into “72” to arrive at the time frame needed.

As an example, using compound interest rates of 6%, you will double your money every 12 years, because 72 divided by 6 equals 12.

One of the great historical investing quotes is from Albert Einstein who said “Compound interest is the eighth wonder of the world. He who understands it earns it, he who doesn’t, pays it.” Although Einstein was not particularly skilled as an investor, he was of course a mathematical genius. He understood that the idea of compounding interest was a way to real wealth.

The idea of compound interest is one of the reasons we here at Wealthplicity are big believers in reinvesting your dividends. Reinvesting dividends will allow you to get more dividends because you own more shares of the company stock then you would if you just accepted the dividend as cash.

Earning dividends on the dividends you earn by reinvesting them to buy more shares is a way to build real wealth. And while it may not seem significant at first, the compounding affect over decades can result in staggering returns for your investment portfolio.

In Summary

One way to build real wealth is to let the compounding effects of interest or dividends work their magic over long periods of time.

“Interest on interest” or “dividends on dividends” is a way to more quickly accumulate wealth, which is a concept that goes back thousands of years.

So by all means if you need the cash, you should collect your interest and dividend payments each month.

However, if you can reinvest the dividends or interest and earn a growing stream of income each year, you will be well rewarded over the long run.

Wealthplicity Recent Posts